Reverse Charge

tags :

Tax #

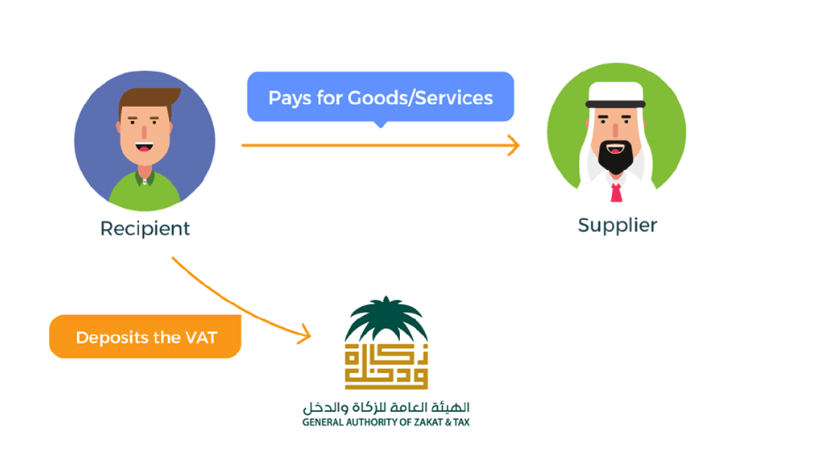

Reverse charge is a mechanism in which the responsibility for reporting and paying tax on a transaction shifts from the supplier to the recipient of the goods or services. This is commonly used in the context of Value Added Tax (VAT) and Goods and Services Tax (GST).

Key Points of Reverse Charge: #

Tax Liability Shift:

- Instead of the supplier charging and remitting VAT/GST to the tax authority, the recipient of the goods or services is responsible for calculating, reporting, and paying the tax.

Purpose:

- The reverse charge mechanism is

typically used to combat tax evasion and to simplify tax administration, especially in cross-border transactions or when dealing with certain types of businesses or services.

- The reverse charge mechanism is

Applicability:

- It applies to specified goods and services as defined by tax regulations and differs from one jurisdiction to another.

- Common sectors include import of services, goods supplied by unregistered vendors, and specific commodities like gold or real estate.

Self-Accounting:

- The buyer (who falls under the reverse charge mechanism) self-accounts for the VAT/GST by declaring

it both as an output tax (tax payable) and, if eligible, simultaneously claiming it as an input tax credit (tax deductible), making the process tax-neutral.

- The buyer (who falls under the reverse charge mechanism) self-accounts for the VAT/GST by declaring

Compliance:

- Businesses must ensure they understand when reverse charge applies to avoid non-compliance, which can result in penalties and interest charges.

Example Scenario: #

A company in Country A (not registered for VAT within Country B) provides consulting services to a business in Country B. Under the reverse charge mechanism:

- The business in Country B must account for the applicable VAT on the consulting services as if it were the supplier.

- The business in Country B reports the VAT amount in its tax return and, if allowed, claims the same amount as input tax, balancing the overall tax liability.

Regulatory Context: #

Different countries have their own laws and specific conditions for reverse charge applicability. For instance, under the European Union VAT system, reverse charge is quite common for cross-border business-to-business (B2B) transactions.

Understanding the reverse charge mechanism is crucial for businesses to ensure proper compliance with tax regulations and efficient tax management.

In Saudi Arabia #

When is reverse charge applied? #

The reverse charge mechanism will be applicable in the following situations:

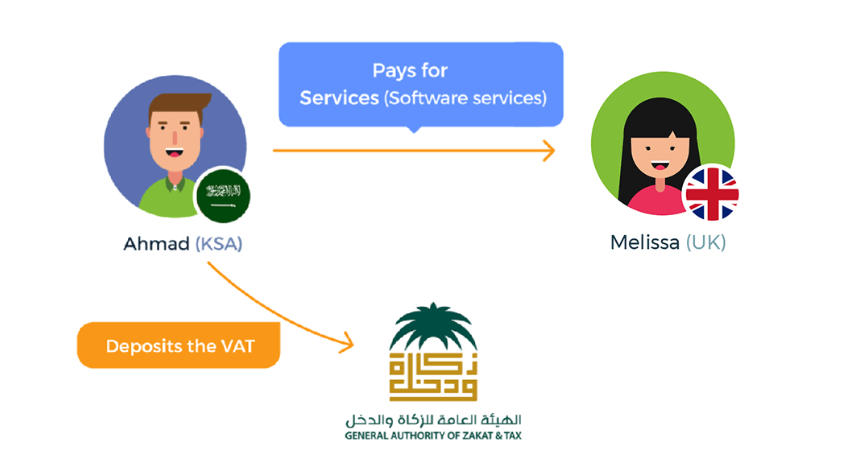

When a VAT-registered business imports a taxable service #

Unlike imported goods, imported services do not go through the Customs Department, so VAT cannot be collected at an airport or a border. Hence, the buyer accounts for input VAT on the transaction using the reverse charge mechanism. To understand the mechanism better, let’s look at an example using an imported service:

Ahmad owns a VAT-registered electronics store in Saudi Arabia. Ahmad’s store uses a software subscription from a UK-based firm owned by Melissa. Since the software is delivered electronically, it never goes through the Customs Department.

Melissa is not registered in Saudi Arabia, so she does not have to file any VAT returns or pay KSA tax. However, Ahmad is a KSA taxpayer and has acquired services from a non-KSA-based software store, so he must record the reverse charge for the transaction on his relevant VAT return.

When a taxable person receives services from a non-resident

#

- From freelancer e.g.

In this case, the taxable person must calculate the amount of VAT due by the reverse charge mechanism.

When the trading occurs within the GCC #

- When trade takes place between GCC states, the supplier is not required to register in the destination country or charge VAT.

- So the buyer needs to account for the VAT under the reverse charge mechanism.

Why is there a need for the reverse charge mechanism? #

The reverse charge mechanism is necessary to apply the domestic tax rate on overseas purchases. This is intended to remove any financial advantage of buying services from overseas compared to domestic purchases.

Industry-specific scenarios #

Online services #

Online services are taxable under the VAT regime. If the recipient of the services is a taxable person, they should pay tax on a reverse charge basis.

If the service provider happens to be a non-resident, they should appoint a representative within the Kingdom, and register for VAT, if their value of sales in KSA is more than 375,000 SAR.

Real estate #

If a VAT-registered person in KSA receives a supply from a non-resident supplier, the supplier is not entitled to charge VAT on the supply. Instead, the recipient should report VAT on their VAT return under the reverse charge mechanism.

The non-resident supplier need not register under the VAT regime to report such supplies, nor do they need to issue VAT compliant tax invoices.

Example: Home LLC, a Qatar-based real estate firm, is charging La Maison WLL, a KSA-based firm, for providing painting and re-structuring services to La Maison’s commercial premises in Jeddah. In this example, Home LLC is a non-residential supplier and La Maison WLL is registered for VAT in KSA. So, it will be the responsibility of La Maison WLL to report VAT on this supply of services.

OCR of Images #

2024-07-21_10-38-51_screenshot.png #

Pays for Goods/Services Recipient Supplier Deposits the VAT Jéallg OL5ju àolell afiall GENERAL AUTHORITY OF ZAKAT & TAX

2024-07-21_10-44-03_screenshot.png #

Pays for Services (Software services) - - - - - - - A 4 EE 3M9 Ahmad (KSA) Melissa (UK) Deposits the VAT = Jéallg 615)u dolcll afiall GENERAL AUTHORITY OF ZAKAT & TAX