Payment Network

tags :

Summary #

- Networks provide the communication system that issuing banks and businesses(merchants) use to process credit card transactions.

- The networks and issuers authorize and process credit card transactions, set the transaction terms, and move payments between customers, businesses, and their banks.

- Major credit card networks include , , American Express, and Discover, but there are others.

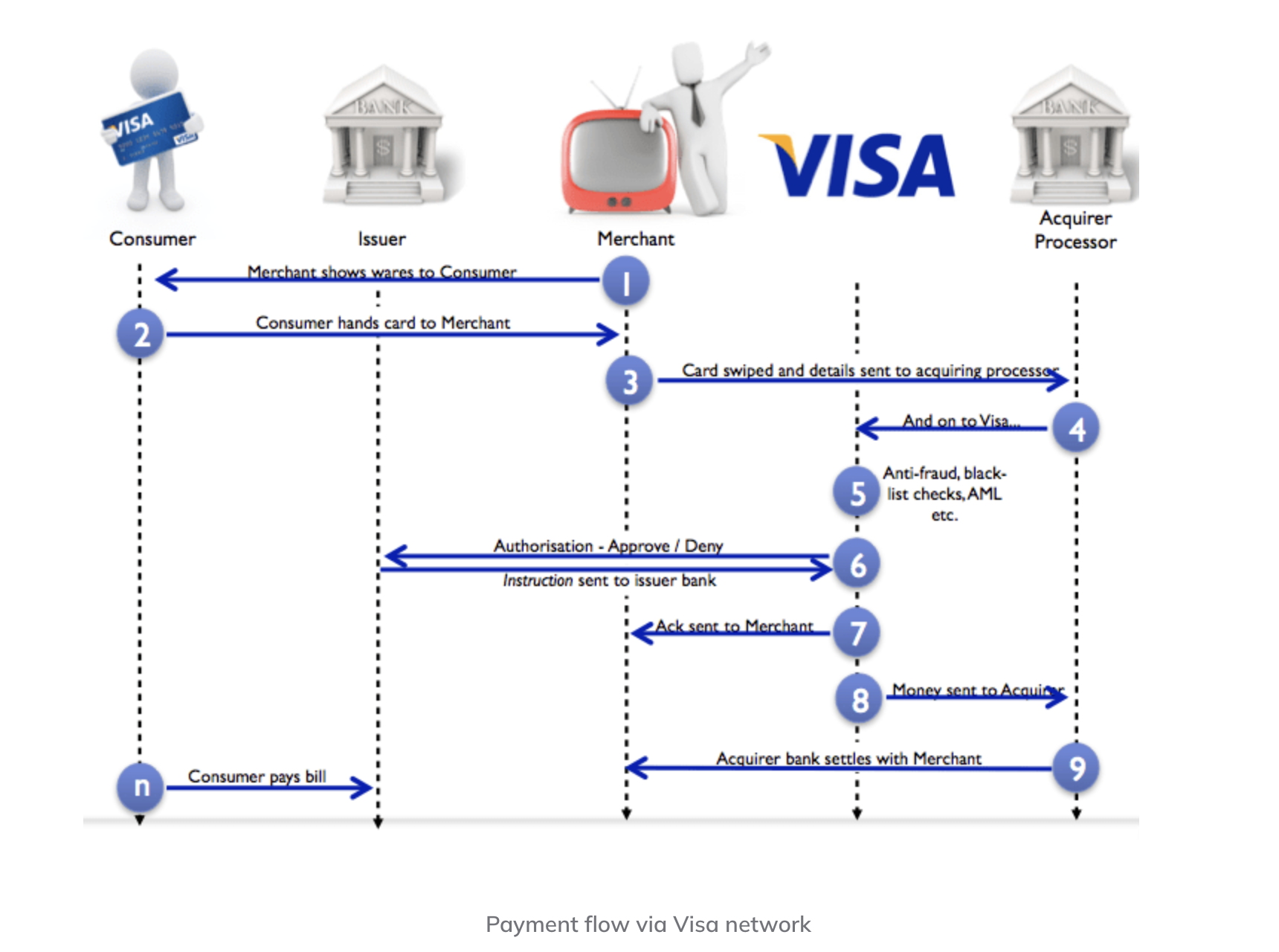

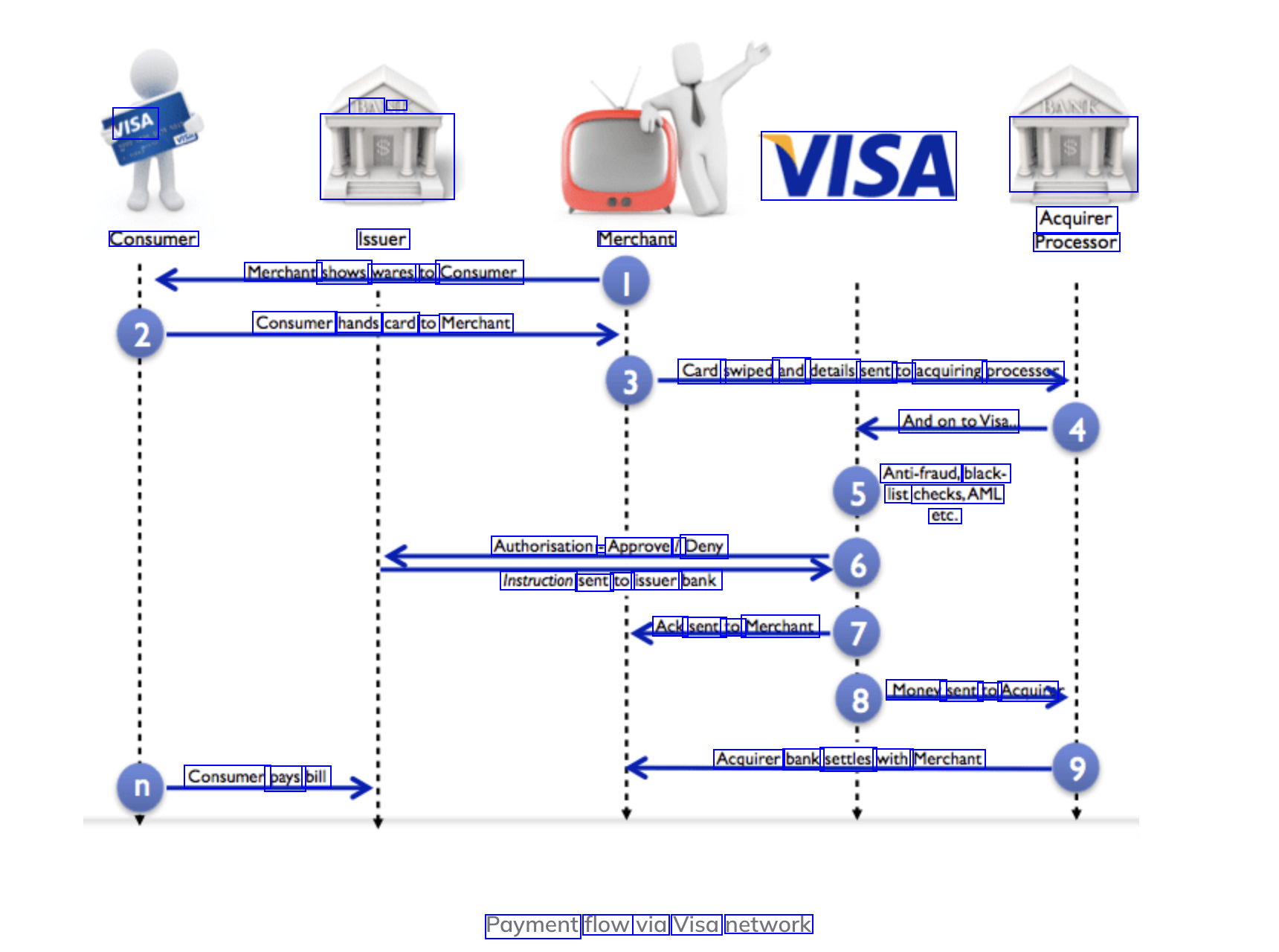

Payment Flow #

Redirects the payment to the Issuing Bank #

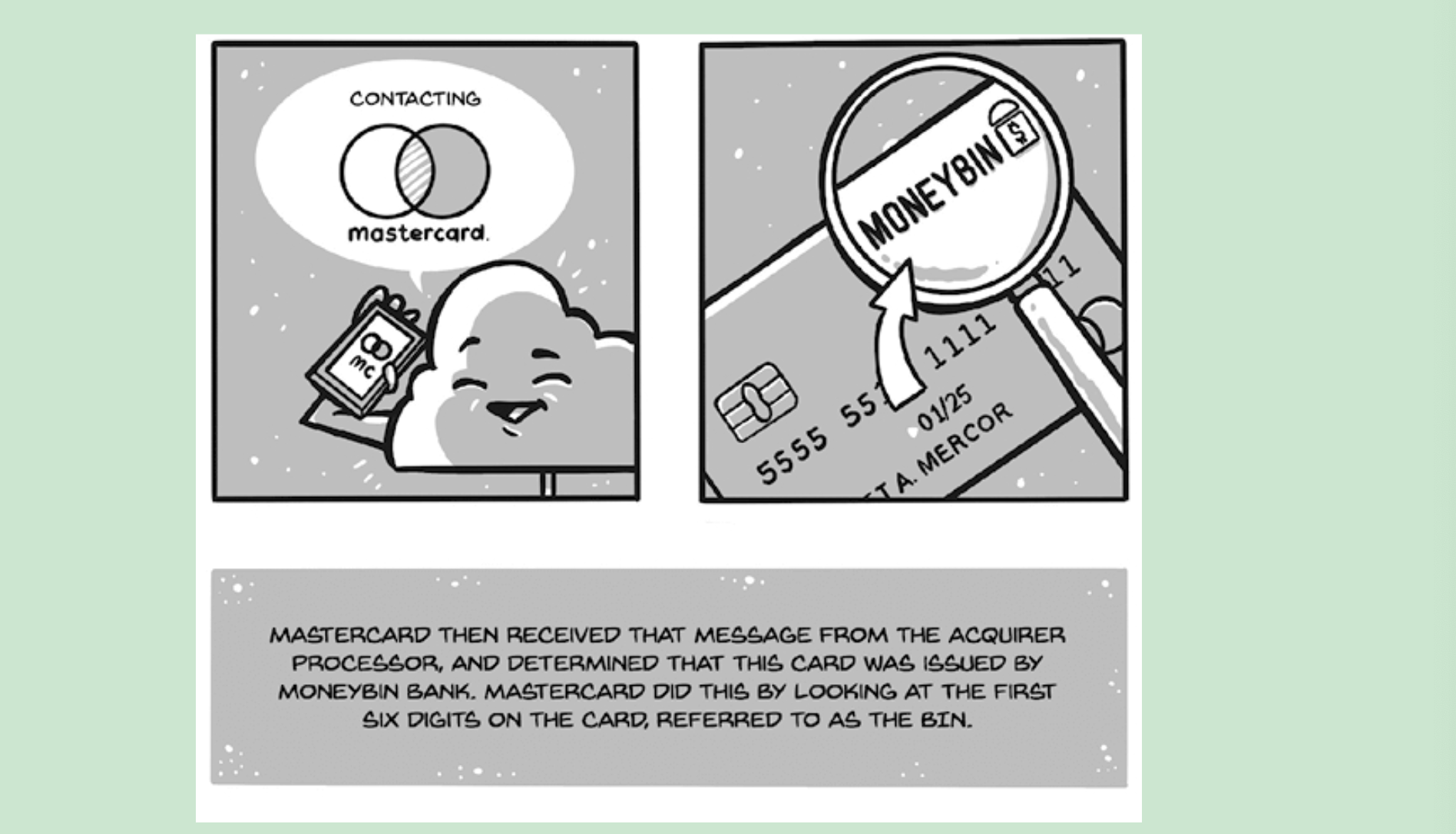

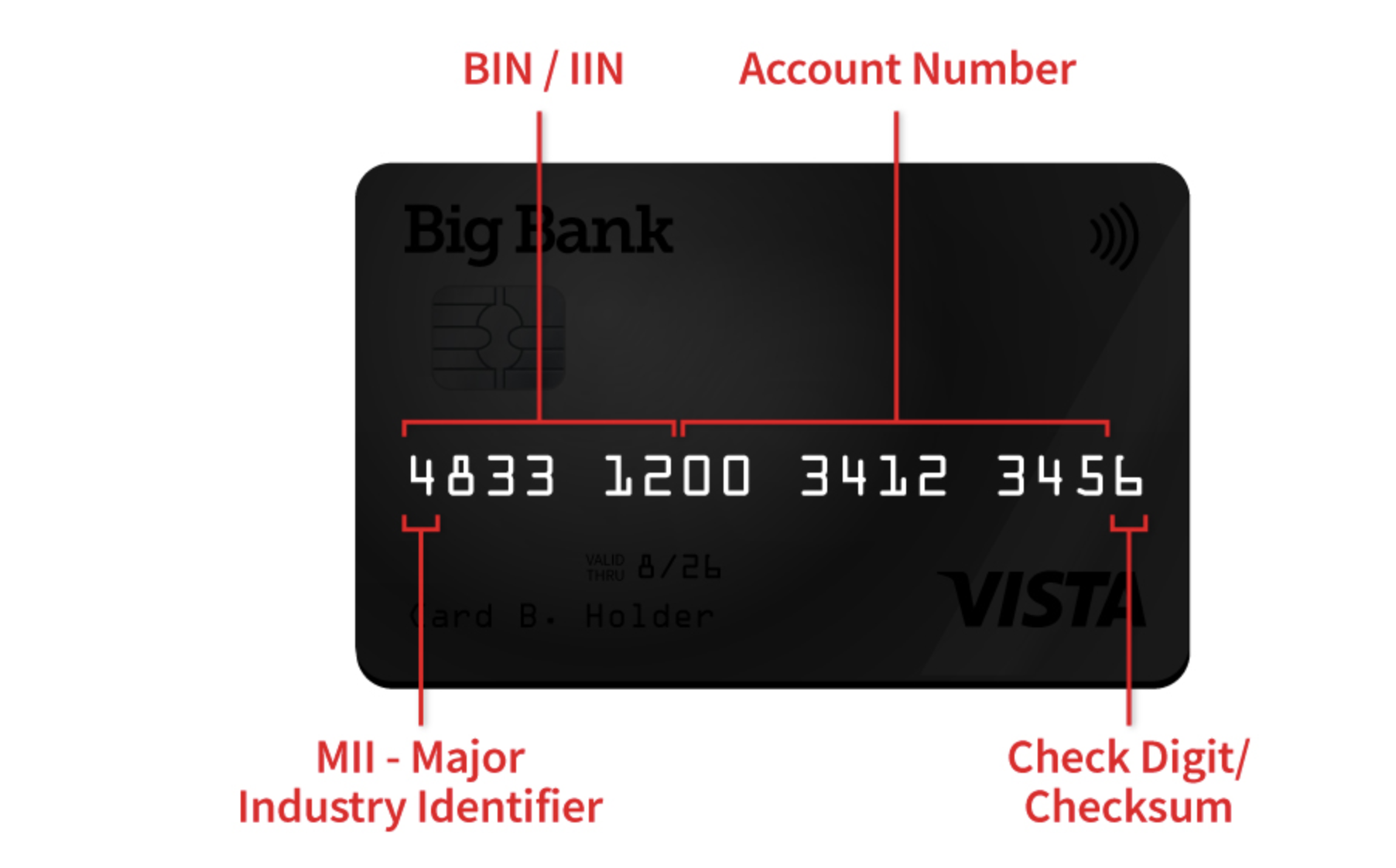

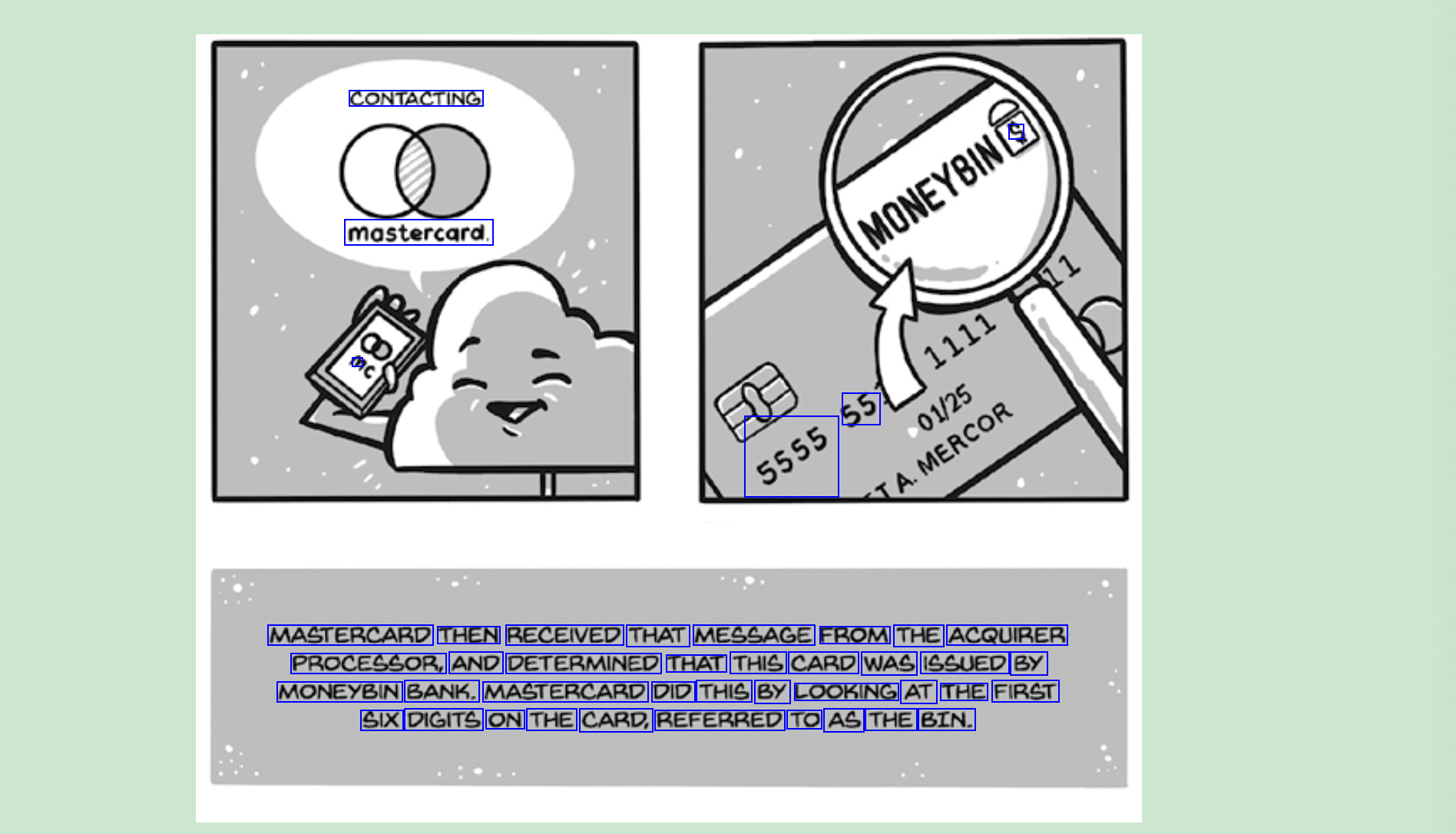

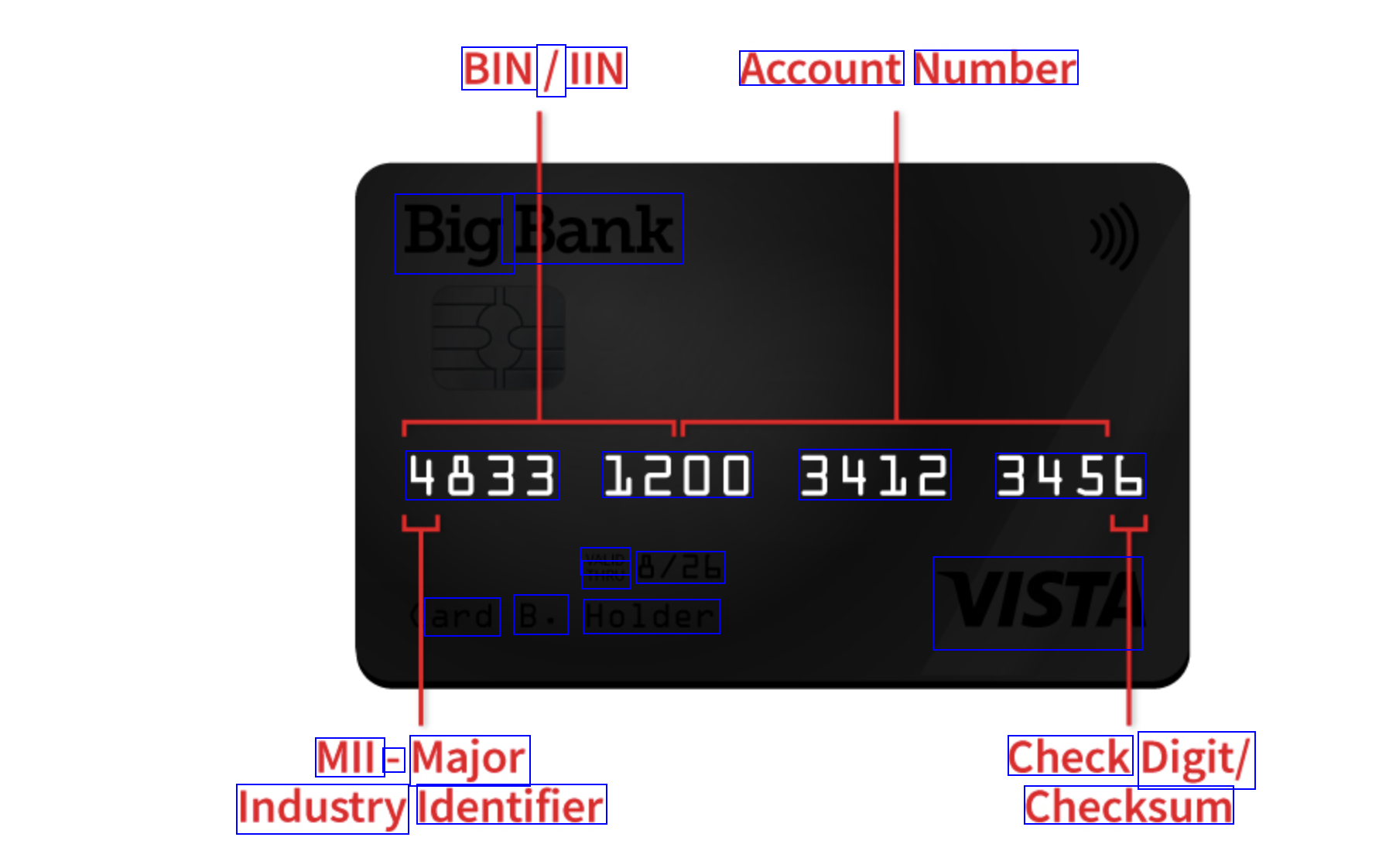

Using first 6 digits of the card, referred to as BIN (Bank Identification Number)

Open Network #

, are open networks

Closed Network #

American Express and Discover typically issue their own cards, are their own bank, and typically provide their own acquiring services.

How they make money? #

Merchants #

A percentage of transaction fee is taken from merchant.

Issuing Bank #

Report settlement fee #

After the transaction has cleared, a reporting settlement fee is typicall charged to the issuer from the card network; Flat per transaction fee.

Per Transaction Fee #

For Authorization and clearing the transaction. Usage fee for transmitting data through the card network “rails”.

Network Rail and Transacting Routing #

Credit Networks (Dual Message) #

- Incurs higher interchange rate.

Debit Network (Single Message) #

Also known as PIN debit purchase

Requires the cardholder to enter the PIN.

Incurs lower interchange rate.

Also knows as Signature purchase

ATM #

Inverse of typical cardswipe: giving money vs taking money, from your own account of-course.

- Will charge user a flat fee per transaction. If the ATM network is included in the banks’ network, this fee will be waived.

8583 #

This is message standard very compact and can travel quickly among the Payment terminal, acquirer processor, network, and the issuer processor.

ISO 8583 is an international standard for financial transaction card originated interchange messaging. It is the International Organization for Standardization standard for systems that exchange electronic transactions initiated by cardholders using payment cards. wikipedia

OCR of Images #

2023-07-02_12-00-45_screenshot.png #

BAU E TAT VISA INT VISA Acquirer Processor Consumer Issuer Merchant Merchant shows wares to Consumer Consumer hands card to Merchant Card swiped and details sent to acquiring processos And.on.toVisa. Anti-fraud, black- list checks,AML etc. Authorisation - Approve / Deny Instruction sent to issuer bank Ack sent to Merchant Money sent to Acauia Acquirer bank settles with Merchant Consumer pays bill Payment flow via Visa network

2023-07-02_12-30-12_screenshot.png #

CONTACTING S mastercard. 2 55 5555 MASTERCARD THEN RECEIVED THAT MESSAGE FROM THE ACQUIRER PROCESSOR, AND DETERMINED THAT THIS CARD WAS ISSUED BY MONEYBIN BANK. MASTERCARD DID THIS BY LOOKING AT THE FIRST SIX DIGITS ON THE CARD, REFERRED TO AS THE BIN.

2023-07-02_12-31-30_screenshot.png #

BIN / IIN Account Number Big Bank 4833 1200 3412 3455 VALID THRU 8/26 ard B. Holder VISTA MII - Major Check Digit/ Checksum Industry Identifier

2023-07-02_14-16-42_screenshot.png #

BUCKS OF STAR OPTIONS CREDIT DEBIT BUCKS OF STAR OPTIONS CREDIT DEBIT ATM

2023-07-02_14-17-18_screenshot.png #

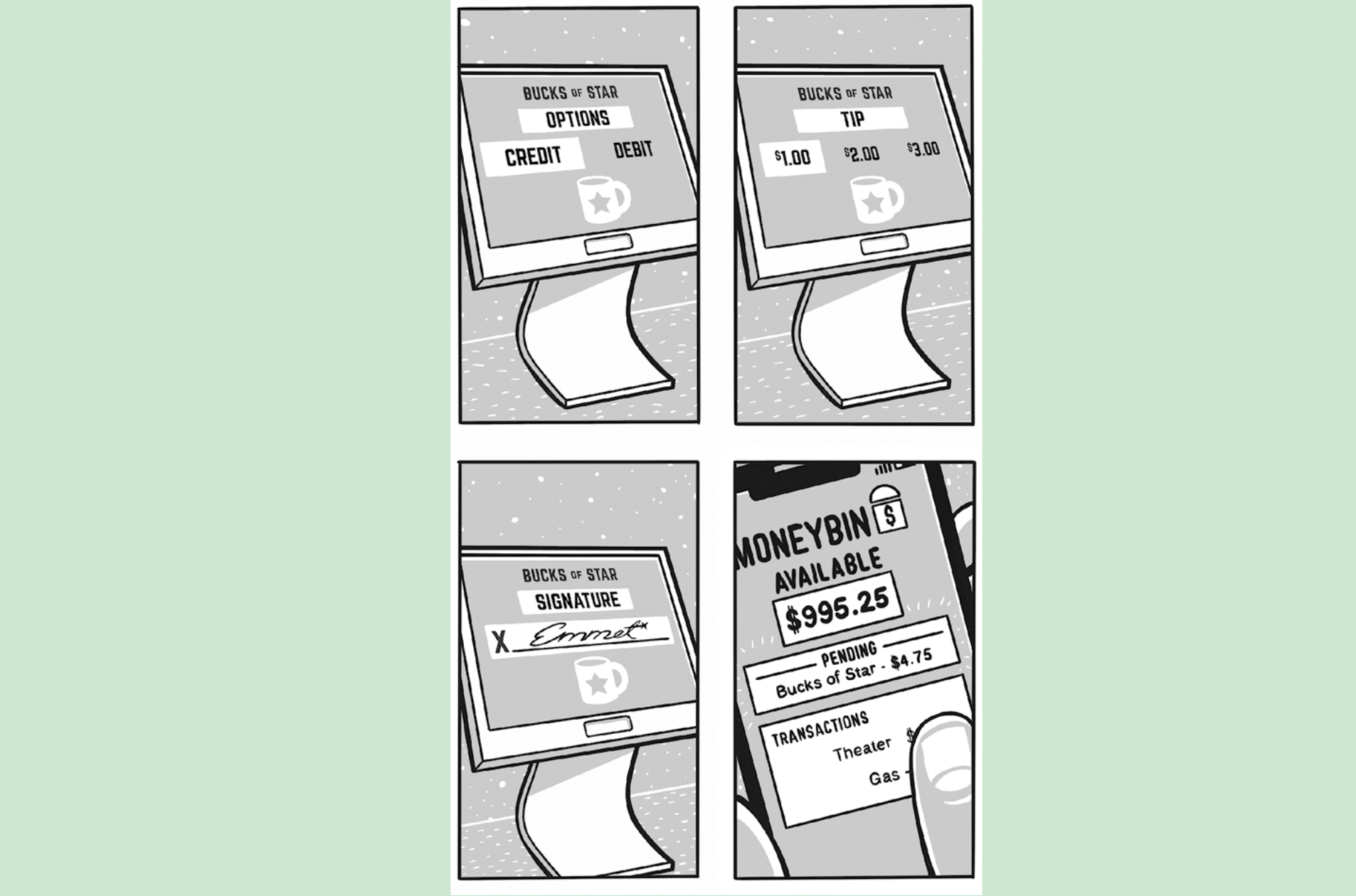

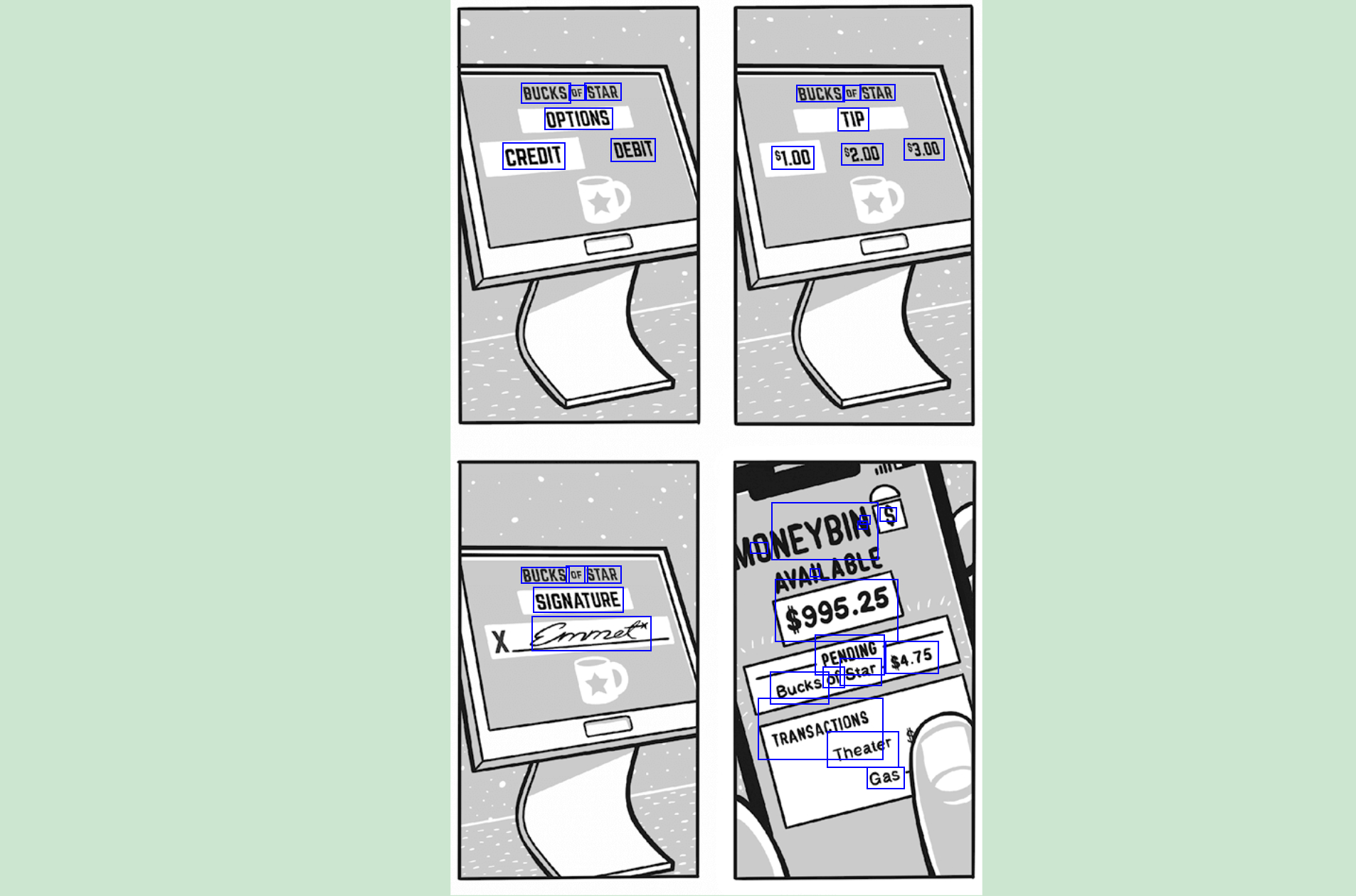

BUCKS OF STAR OPTIONS CREDIT DEBIT BUCKS OF STAR TIP $1.00 $2.00 $3.00 - a S 11 NEYBIN - $995.25 BUCKS OF STAR SIGNATURE Emmet PENDING $4.75 of Star Bucks FHRAENEITONE Theater Gas

2023-07-02_14-19-42_screenshot.png #

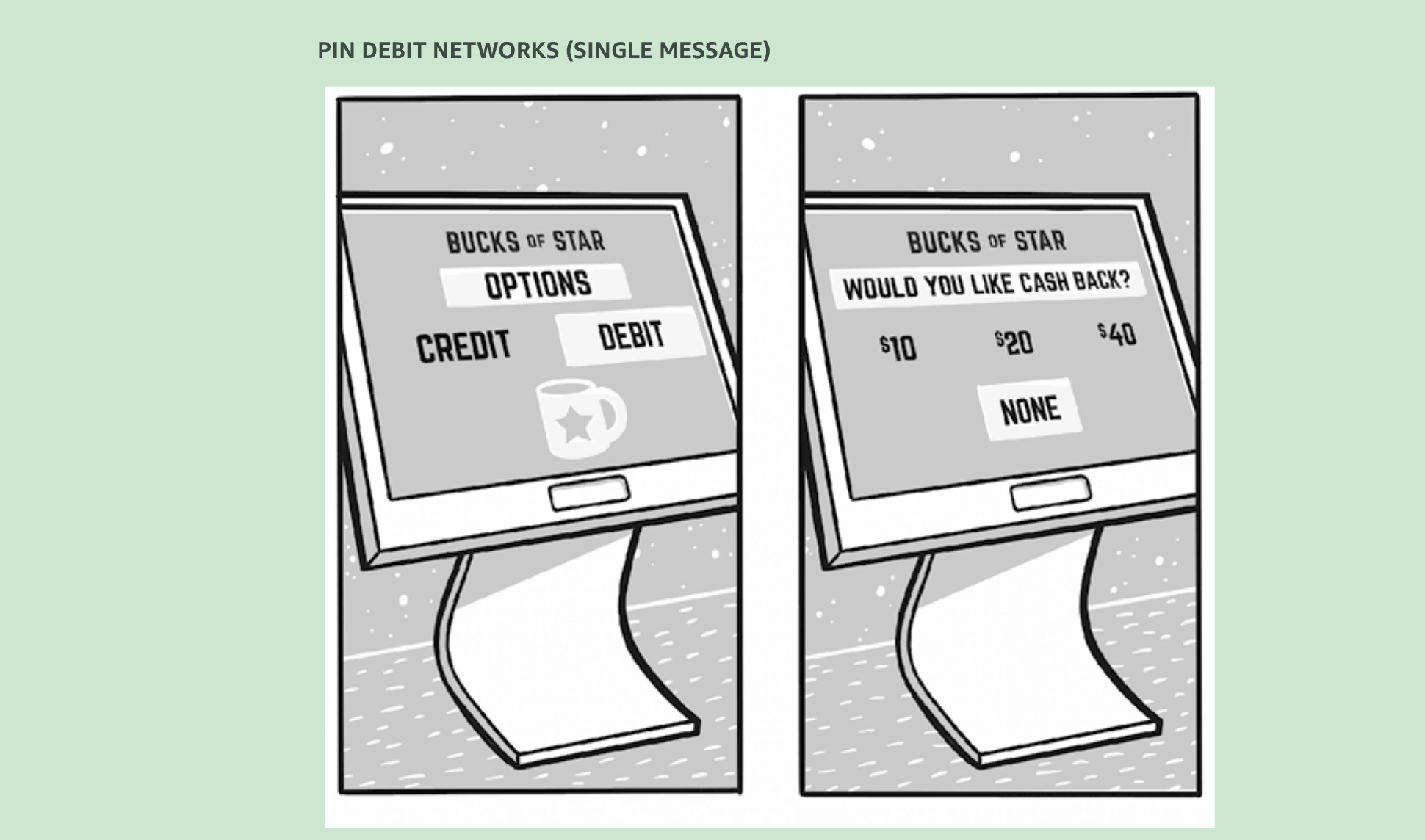

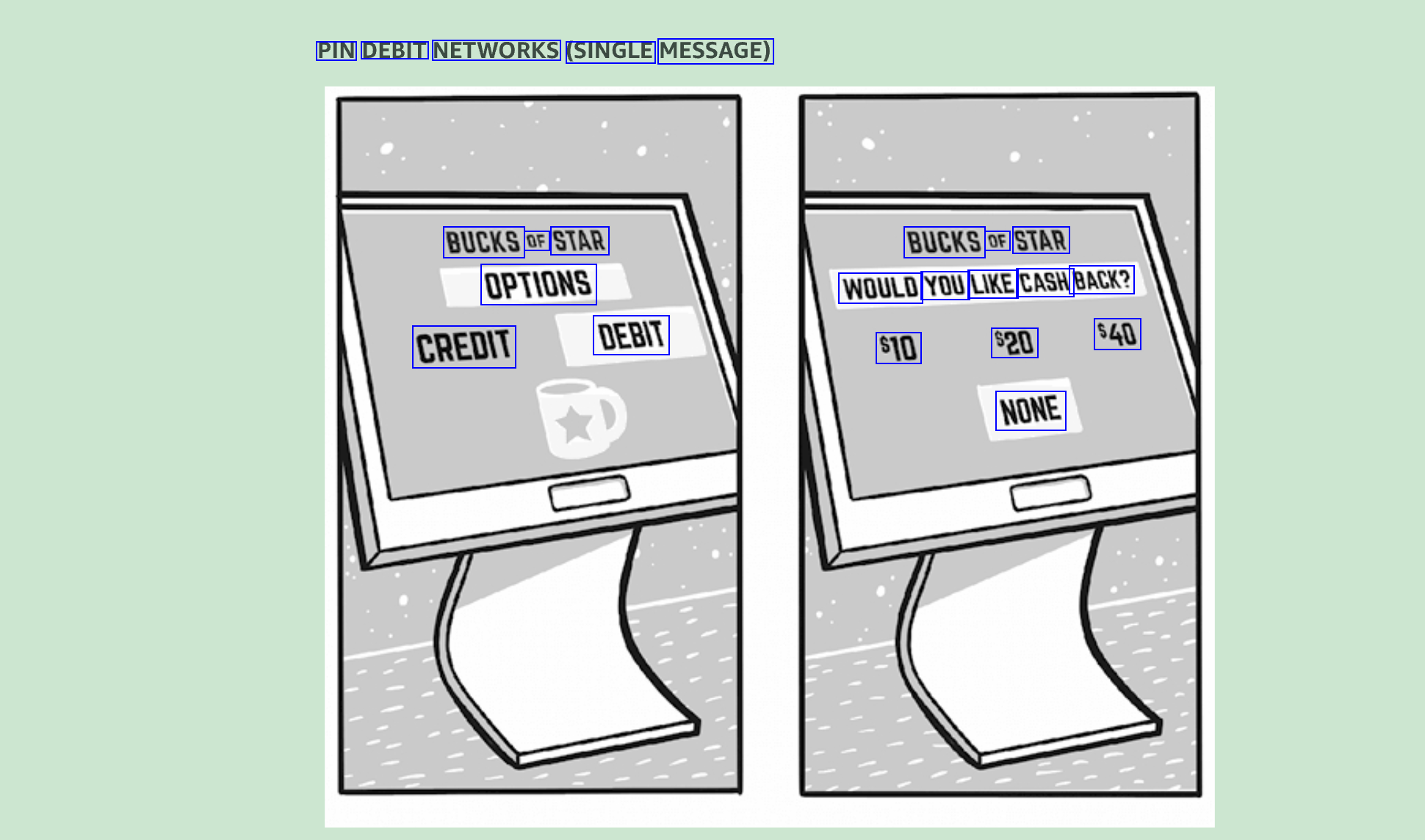

PIN DEBIT NETWORKS (SINGLE MESSAGE) BUCKS OF STAR OPTIONS BUCKS OF STAR WOULD YOU LIKE CASH BACK? CREDIT DEBIT S10 $20 $40 NONE

2023-07-02_14-21-03_screenshot.png #

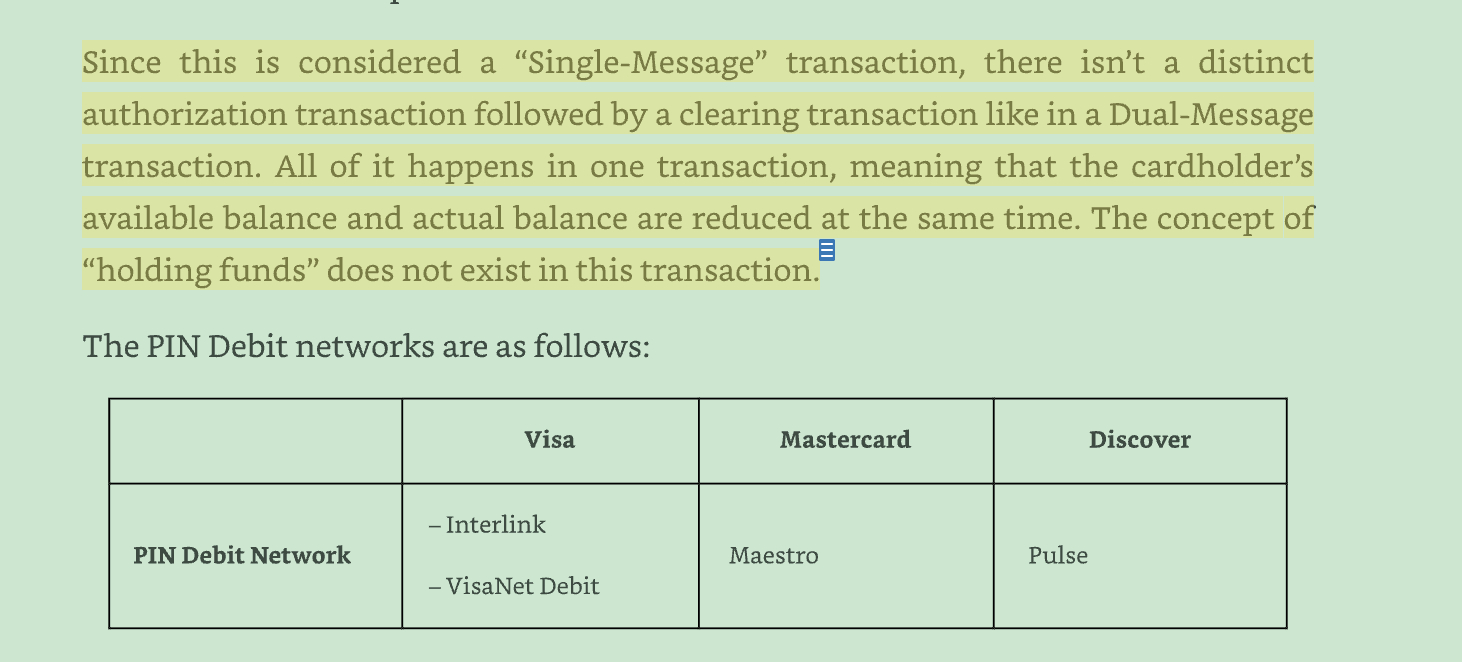

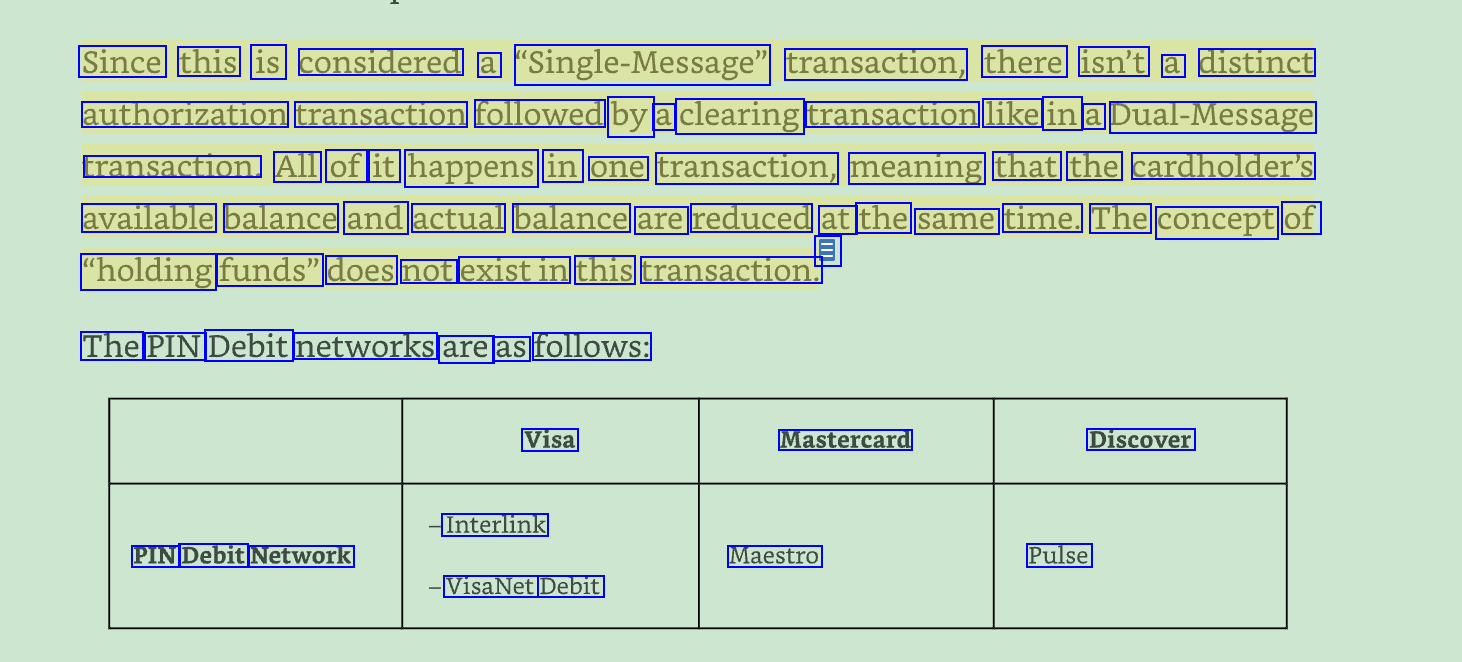

Since this is considered a "Single-Message" transaction, there isn't a distinct authorization transaction followed by a clearing transaction like in a Dual-Message transaction. All of it happens in one transaction, meaning that the cardholder's available balance and actual balance are reduced at the same time. The concept of E "holding funds" does not existin this transaction. The PIN Debit networks are as follows: Visa Mastercard Discover Interlink PIN Debit Network Maestro Pulse VisaNet Debit

2023-07-02_14-22-23_screenshot.png #

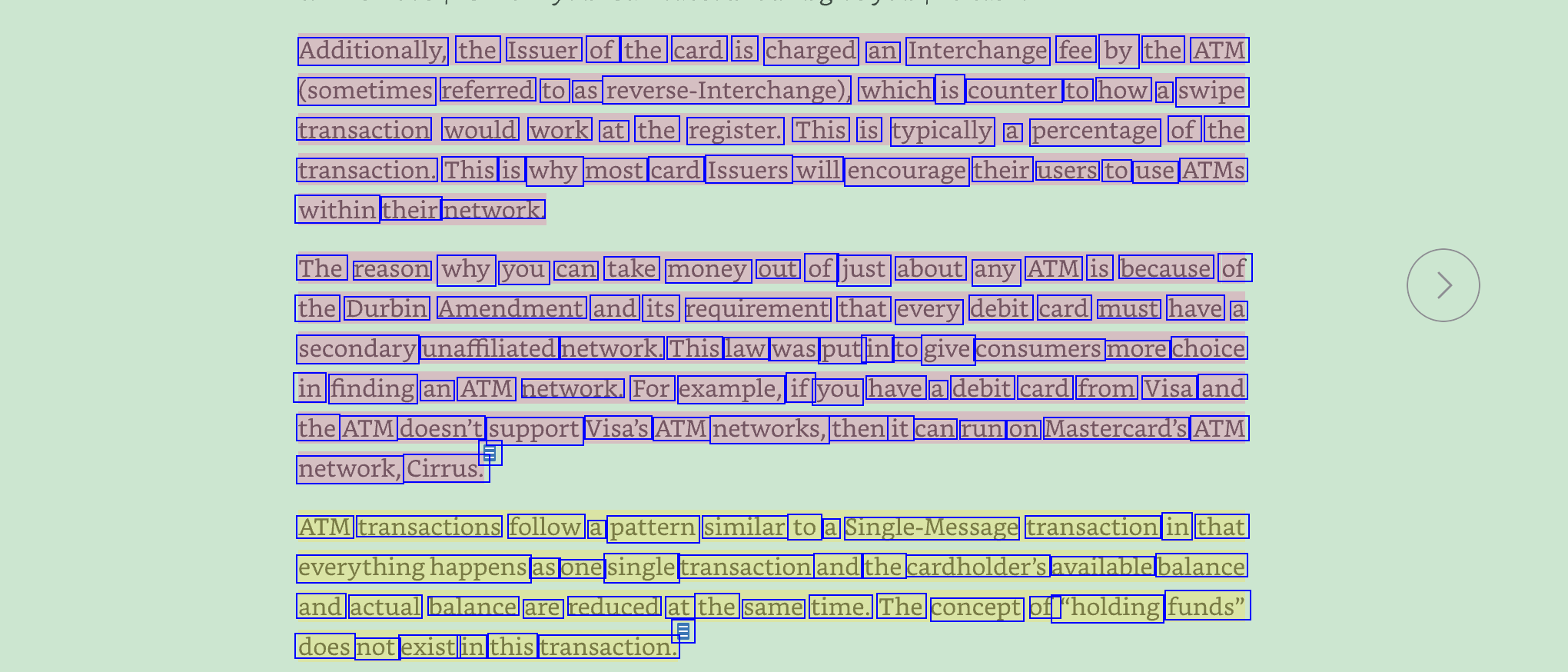

Additionally, the Issuer of the card is charged an Interchange fee by the ATM (sometimes referred to as reverse-Interchange, which is counter to how a swipe transaction would work at the register. This is typically a percentage of the transaction. This is why most card Issuers will encourage their users to use ATMs within their network. The reason why you can take money out of just about any ATM is because of the Durbin Amendment and its requirement that every debit card must have a secondary unaffiliated network. This law was put in to give consumers more choice in finding an ATM network. For example, if you have a debit card from Visa and the ATM doesn't support Visa's ATM networks, then it can run on Mastercard's ATM E network, Cirrus. ATM transactions follow a pattern similar to a Single-Message transaction in that everythinghappens as one single transaction and the cardholder's available balance and actual balance are reduced at the same time. The concept of "holding funds" E does not exist in this transaction.

2023-07-02_14-24-17_screenshot.png #

Visa Mastercard Discover ATM Network Plus Cirrus Pulse