Open Banking Use Cases

Summary #

- tags

- Open Banking

Applications #

How UK consumers are using Open Banking? #

From this report published in Sept, 2021 Consumers using AIS : 62% Consumers using PIS : 27%

Account Aggregation 34% #

To view all bank accounts in one place – 34%

PFM 28% #

To keep an eye on all savings and investments – 28%

Transactions 27% #

To move money between bank accounts and savings – 27%

Survey report by Tink #

ref Done in 2019 and 2020 in Europe, by interviewing 290 financial executives from 12 countries.

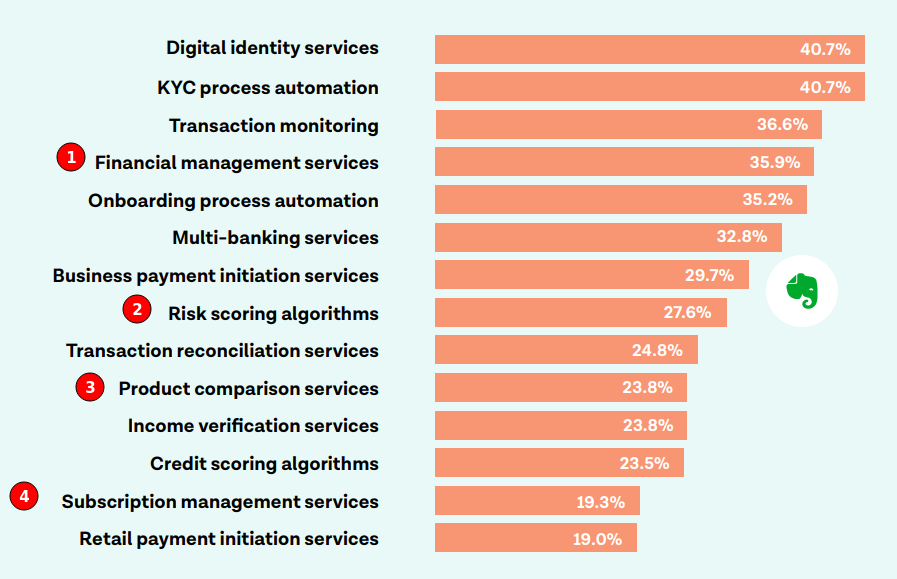

Digital identity services #

- Strong customer authentication is a legal requirement of PSD2

- requires to identify customer by providing authentication methods.

KYC Process Automation #

(Know Your Customer Process Automation)

- additional accounts associated with customers.

- Names and accounts registered by this user

- Fetch and verify customer information

Transaction Monitoring #

- requirements for

- To enable PSP to detect fraudulent or unauthorized transactions

- Profile of customer

- Help in identifying abnormal activity

Financial Management Services #

- By aggregating financial information from different accounts and banks, open banking can revolutionize money management for consumers and financial planning for businesses

- PFM

- Business get more transparency by collecting data from different banks and jurisprudence by collecting data into to a single information systems.

Onboarding automation #

Open banking can help users automatically fill these applications by aggregating their data, reducing the hassle and stress. This makes the onboarding experience a lot smoother, or even effortless

Multi-banking #

Single interface to interact with multiple bank accounts.

Business payment initiation services #

Business payment initiation is focused on giving businesses the ability to pay invoices or make transfers in a fast and intuitive manner without needing to pay unnecessary transaction fees

Payments can be started from ERP or their own software

Risk scoring algorithms #

By aggregating account information, various risk scores can be calculated – from credit risk (e.g. binary debt score),

- to insurance risk,

- or even health risks (by analysing the spending on gambling or unhealthy habits).

Depending on the service at hand, it can accelerate the onboarding for a service process dramatically.

Transaction reconciliation services #

Product comparison services #

With access to a customer’s complete financial footprint, it’s possible to estimate the interest rates and service fees that are charged for their financial products (like investment account, mortgage, loan, insurance). Banks can choose to prompt a customer to see if there is an interest in a more affordable solution or alternative offering.

Income verification services #

Many financial companies need to be able to verify income in order to assess whether a customer is eligible for a particular service. It’s also an important component of the risk assessment. By being able to verify income, salary, and potentially even employer, financial institutions can design services that are better, quicker, and more tailored to the individual.

Credit scoring algorithms #

Beyond risk assessments, open banking can be used to enhance credit scoring algorithms. Not just by fetching up-to-date account information, but by allowing a customer to provide access to their full financial situation in order to get access to a loan.

Subscription management services #

An emerging use case where a financial institution operates as a concierge(caretaker) and helps the user by renegotiating subscription fees, activating new subscriptions, or cancelling subscriptions on the customer’s behalf.

Retail payment initiation services #

The payment landscape is booming and retailers are being flooded with new payment options. However, many payment options are considered expensive and payment initiation can provide a more affordable alternative. In addition, payment initiation services have applications for both point-of-sale and online payments.

AIS use cases #

Risk assessment #

- To predict customers behavior from risk’s perspective

- remote financial verification

How does it work?

Combine AIS data from multiple banks + AI/ML

Scoring model

Using AI and ML

- Credit card risk assessment

- Shopping preferences

Probability of insolvency

- protect business clients from unreliable consumers

Customized assessments

according to the clients requirement from the data

Example of a company

We rely on Mastercard’s infrastructure. This means that we provide access to customer data from the 15 largest banks in Poland, including

- PKO BP

- Pekao SA

- Millenium

- Credit Agricole

- mBank

- ING

- Alior Bank

- BNP Paribas

- Bank Pocztowy

- Santander

- BOŚ Bank

On special request, we may also obtain data from customers of banks located outside Poland.

Services offered

Identity verification

verify data provided by the customer with actual data

Customer profile

- subscriptions maintained (Project X)

- dues paid on time

- due loans

- shopping habits (Project X)

- other relevant info

Income

- amount

- regularity

Financial market activity

- analysis related to the credits and loans

Skip tracking

- additional contact number

Geo location

- where transaction happened

B2B client report

- List of contractors

- Sales concentration and stability

- Cash flow analysis

- Negative events such as bailiff’s seizures

Financial verification

- Creditworthiness of customer

The flow

Client: Banks or Loan companies or Telecom companies Service provider: AIS service provider who is doing risk assessments

- Customer wants some service that requires verification of his credit worthiness and financial

- Customer visits the application(web or mobile) of their clients

- The client decides what information of customer is needed and asks their consent to fetch the sensitive data

- From AIS open banking

- From service provider’s partner network

- Customer gets redirected to the Bank’s login to authorize

- Service provider verifies and concludes the process

- The end result is a contract with Telecommunication company to by installment based mobile phone

- It can B2B contracts that requires financial verification

BNPL Tabby and Tamara they ask for credit/debit card as surety for risk

Forecast of consumer behavior

Use data to forecast behavior and risk associated with it

Who do they work for?

- Banks

- Insurance companies

- Loan companies

- Telecommunication operators

- Real estate agencies

- Companies based on sharing economies