Open Banking

Summary #

- tags

- ,

- OBIE

- Open Banking Implementation Entity

Projects #

Project X is planning to use open banking. https://www.vfsglobal.com/en/individuals/index.html

#

Accounts #

Balances #

Transactions #

Around the World #

India #

Called Unified Payments Interface (UPI)

UPI #

Account Aggregator (AA) #

UPI is a digital payment system through which a user can both send and receive money through a Virtual Payment Address (VPA). The money will be directly debited from the customer’s bank account. ref

UPI enables PIS (Payment Initiation Service)

India’s Unified Payments Interface (UPI), which enables third-party initiated payments (PIS) through a centralized API framework, has been used to drive the digitisation of payments and movement of money with phenomenal success. As of November 2020, UPI transaction volume had reached the 2 billion mark, representing 10% of India’s GDP. ref

Apps providing UPI feature

PhonePe

Paytm

BHIM app

MobiKwik

Google pay

Uber

Chillr

Paytm Payments Bank

SBI Pay

iMobile

Axis Pay

Bank of Baroda (BOB) UPI

An Account Aggregator (AA) is a type of RBI regulated entity (with an NBFC-AA license) that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network. Data cannot be shared without the consent of the individual.

UK #

Open Banking Standard Specifications

AIS API specifications #

Transactions Balances Accounts

EU (EEA) #

Called PSD2 (Payment services directive 2)

Open Banking Map #

http://www.openbankingmap.com/

Advantages of Open Banking over Traditional Banking #

Summary #

- Faster and easier

- Secure

- Less expensive to customer

Details #

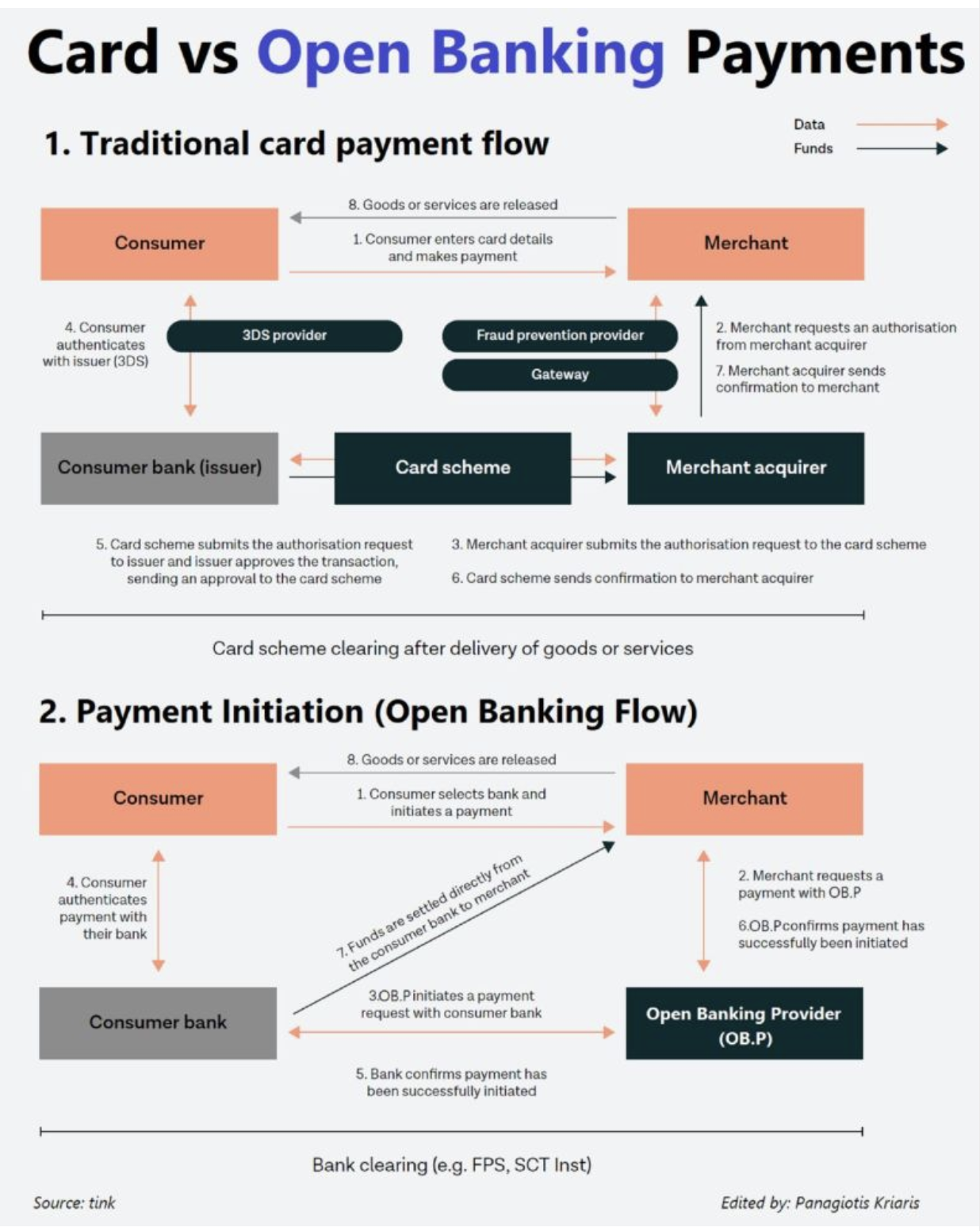

Demand for faster payments (because OB payments are nearly instant and settle faster than card transactions, giving merchants a clearer picture of their cash flow). The below graph from Tink brilliantly captures that showing the difference in the payment flow.

Push for tighter payment security (OB payments are inherently more secure than other digital payments because no personal payment details are shared between the customers and merchants)

Card fee tensions (Open Banking payments let merchants avoid paying interchange fees - the fees merchants pay to accept card payments, which are set by card networks like Visa and Mastercard).

Glossary #

#

#

#

PSU #

Payment Service User’s

TSP #

Technical Service Providers (TSPs)

are companies which work with regulated providers to deliver open banking products and services.

Companies to benchmark #

https://plaid.com/ https://truelayer.com/data/

More competitors of tink https://craft.co/tink/competitors https://www.paylead.fr/

Open Banking vs #

With fees as low as 0.19%, open banking is cementing Yotta Pay’s status as an ethically-driven payments provider, when compared with fee that ranges between 1-3.5%.

Relation between and Open Banking #

Open Banking and GDPR (General Data Protection Regulation) are both regulatory that relate to the handling of personal data and financial information. Here’s the relationship between Open Banking and GDPR:

Common Goal of Data Protection #

GDPR and Open Banking both aim to protect consumers’ personal data. GDPR focuses on safeguarding personal data in all industries, while Open Banking specifically addresses data sharing and access in the financial sector. ref

Data Control #

GDPR grants individuals control over their personal data, allowing them to determine how it is collected, processed, and used. Similarly, Open Banking emphasizes giving consumers control over their financial data when sharing it with third-party providers.

Data Portability #

Open Banking aligns with GDPR’s principles of data portability. It facilitates the secure sharing of financial data between banks and authorized third parties, ensuring compliance with GDPR requirements for data transfer[5].

Risk Mitigation #

While some argue that Open Banking poses risks to personal data, proponents assert that it aligns with data protection legislation’s goals, such as GDPR, in promoting secure data sharing and access[4].

In summary, Open Banking and GDPR share common objectives of data protection and consumer control over personal information. Open Banking is designed to be compatible with GDPR principles and requirements, ensuring that financial data sharing is done securely and in compliance with data protection regulations.

OCR of Images #

2023-02-06_22-28-39_screenshot.png #

Card VS Open Banking Payments Data Funds 1. Traditional card payment flow 8. Goods or services are released 1.Consumer enters card details and makes payment Consumer Merchant 4. Consumer authenticates with issuer (3DS) 3DS providor Fraud prevention providor Gateway 2. Merchant requests an au from merchant acquirer 7.Merchant acquirer send confirmation to merchant Consumer bank (issuer) Card scheme Merchantacquirer 5. Card scheme submits the authorisation request 3. Merchant acquirer submits the authorisation request to the card to issuer and issuer approves the transaction, sending an approval to the card scheme 6. Card scheme sends confirmation to merchant acquirer Card scheme clearing after delivery of goods or services 2. Payment Initiation (Open Banking Flow) 8. Goods or services are released 1. Consumer selects bank and initiates a payment Consumer Merchant from dretl to ale vecindi are bank nruidae -al tne 4. Consumer authenticates payment with their bank 2. Merchant requests with OB.P payment 6.OB.Pconfirms paym successfully been init 3.0B.Pinitiates a payment request with consumer bank 5. Bank confirms payment has been successfully initiated Consumer bank Open Banking Provider (OB.P) Bank clearing (e.g. FPS, SCT Inst) Source: tink Edited by: Panagiotis

2023-07-02_16-39-23_screenshot.png #

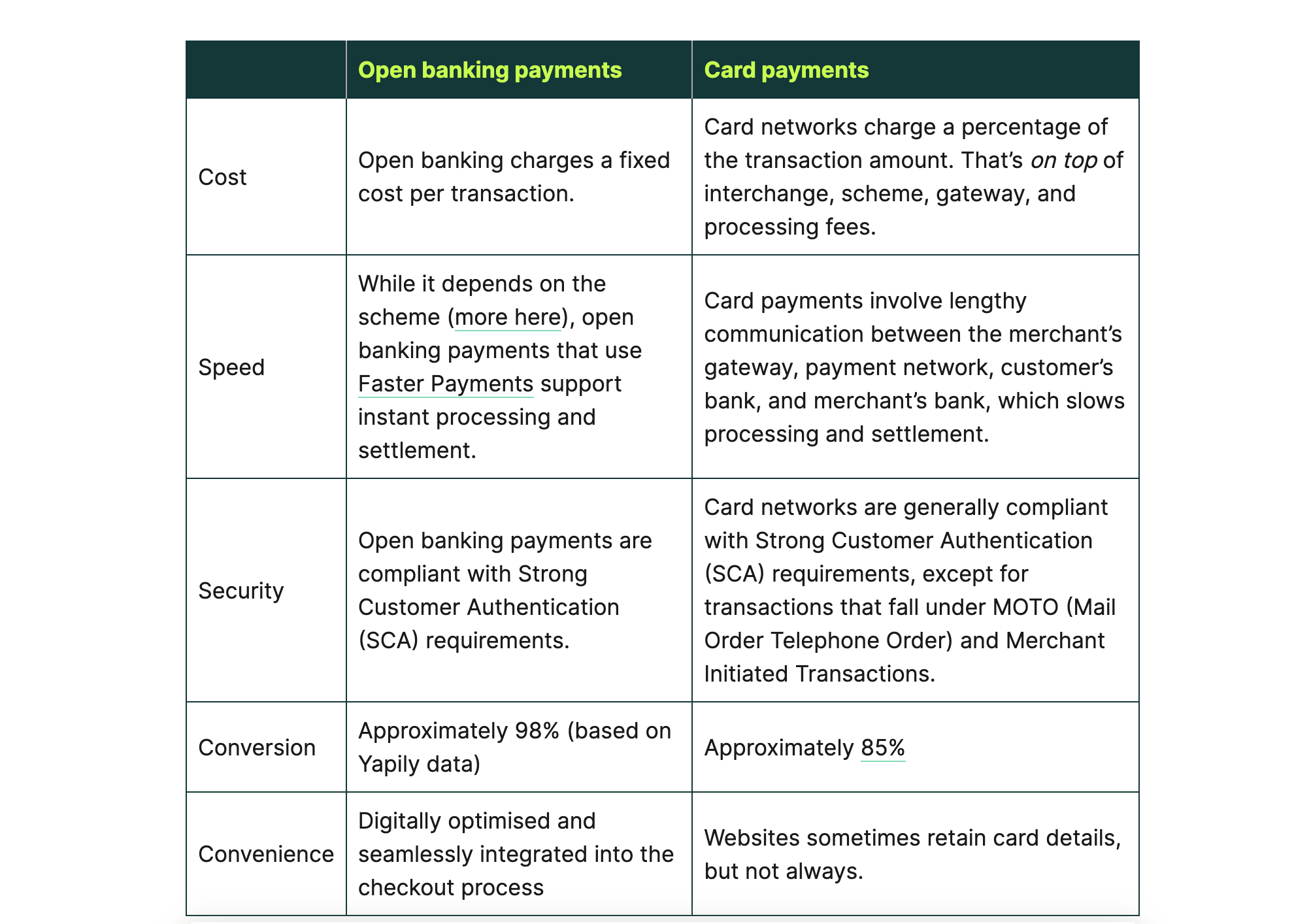

Open banking payments Card payments Card networks charge a percentage of Open banking charges a fixed the transaction amount. That's on top of Cost cost per transaction. interchange, scheme, gateway, and processing fees. While it depends on the scheme (more here), open banking payments that use Faster Payments support instant processing and settlement. Card payments involve lengthy communication between the merchant's gateway, payment network, customer's bank, and merchant's bank, which slows processing and settlement. Speed Card networks are generally compliant with Strong Customer Authentication (SCA) requirements, except for transactions that fall under MOTO (Mail Order Telephone Order) and Merchant Initiated Transactions. Open banking payments are compliant with Strong Customer Authentication (SCA) requirements. Security Approximately 98% (based on Conversion Approximately 85% Yapily data) Digitally optimised and Websites sometimes retain card details, Convenience seamlessly integrated into the but not always. checkout process

OCR of Images #

2023-02-06_22-28-39_screenshot.png #

Card VS Open Banking Payments Data Funds 1. Traditional card payment flow 8. Goods or services are released 1.Consumer enters card details and makes payment Consumer Merchant 4. Consumer authenticates with issuer (3DS) 3DS providor Fraud prevention providor Gateway 2. Merchant requests an au from merchant acquirer 7.Merchant acquirer send confirmation to merchant Consumer bank (issuer) Card scheme Merchantacquirer 5. Card scheme submits the authorisation request 3. Merchant acquirer submits the authorisation request to the card to issuer and issuer approves the transaction, sending an approval to the card scheme 6. Card scheme sends confirmation to merchant acquirer Card scheme clearing after delivery of goods or services 2. Payment Initiation (Open Banking Flow) 8. Goods or services are released 1. Consumer selects bank and initiates a payment Consumer Merchant from dretl to ale vecindi are bank nruidae -al tne 4. Consumer authenticates payment with their bank 2. Merchant requests with OB.P payment 6.OB.Pconfirms paym successfully been init 3.0B.Pinitiates a payment request with consumer bank 5. Bank confirms payment has been successfully initiated Consumer bank Open Banking Provider (OB.P) Bank clearing (e.g. FPS, SCT Inst) Source: tink Edited by: Panagiotis

2023-07-02_16-39-23_screenshot.png #

Open banking payments Card payments Card networks charge a percentage of Open banking charges a fixed the transaction amount. That's on top of Cost cost per transaction. interchange, scheme, gateway, and processing fees. While it depends on the scheme (more here), open banking payments that use Faster Payments support instant processing and settlement. Card payments involve lengthy communication between the merchant's gateway, payment network, customer's bank, and merchant's bank, which slows processing and settlement. Speed Card networks are generally compliant with Strong Customer Authentication (SCA) requirements, except for transactions that fall under MOTO (Mail Order Telephone Order) and Merchant Initiated Transactions. Open banking payments are compliant with Strong Customer Authentication (SCA) requirements. Security Approximately 98% (based on Conversion Approximately 85% Yapily data) Digitally optimised and Websites sometimes retain card details, Convenience seamlessly integrated into the but not always. checkout process