Chargeback

tags :

Summary #

- When a cardholder doesn’t recognize a charge on a Credit Card or Debit Card, they may request their money back through their Issuing Bank.

- Chargeback can also be used in case goods and services have not been provided by the Merchant, but the merchant refuses to return the money.

- This step will happen after settlement.

Zero Liability Policy #

- If the cardholder did not do the payment, then he is not responsible for the payment - they will get the refund.

- Cardholder will get new card and will have to update his card.

- Ultimately the Issuer bank will decide about the liability: whether to charge the cardholder or absorb it.

Chargeback flow #

Disputing the Chargeback #

EMV Chip not used #

If merchant uses magnetic swipe instead of EMV chip, the liability lies with Merchant for the chargeback: for using less secure way for the purchase.

Online Transactions - CVV #

3D Secure #

Chargeback rate to avoid penalties #

Preventing Chargebacks #

OCR of Images #

2023-07-02_14-02-06_screenshot.png #

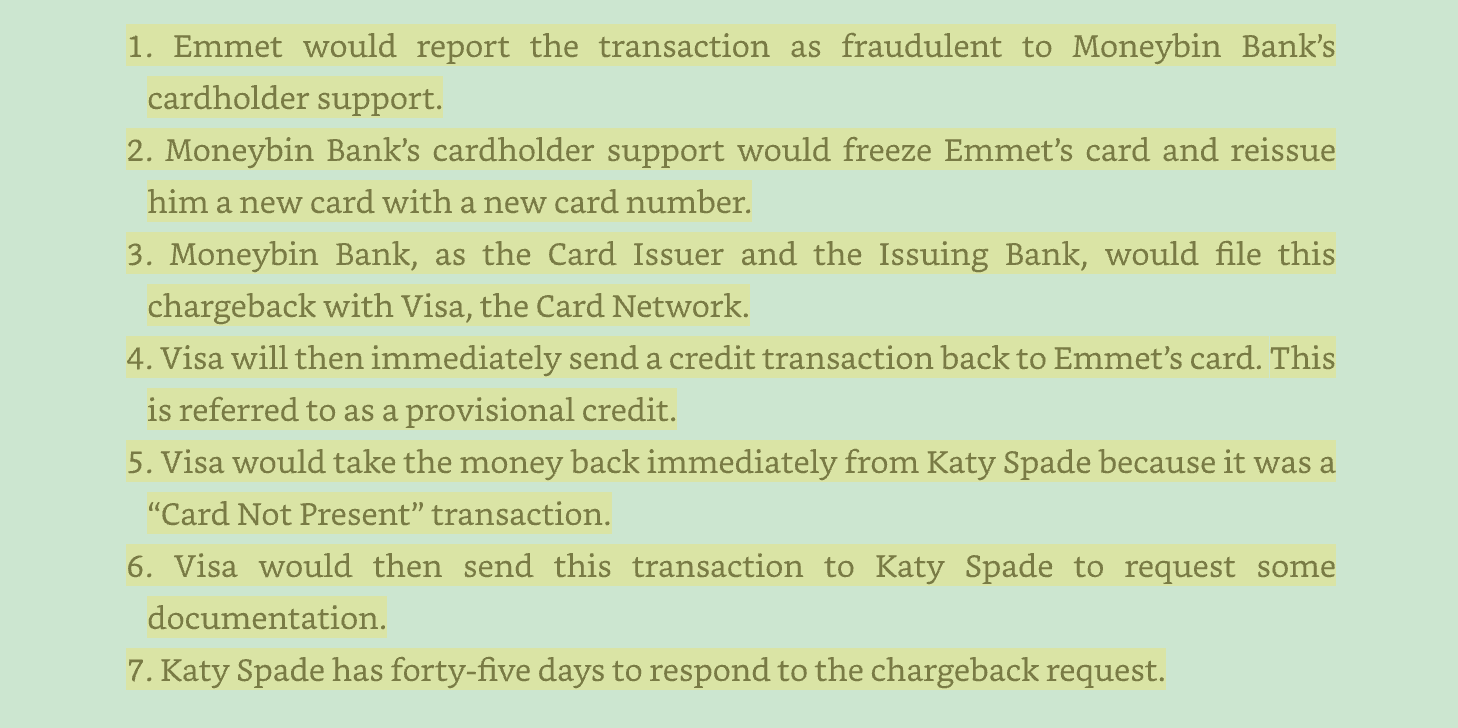

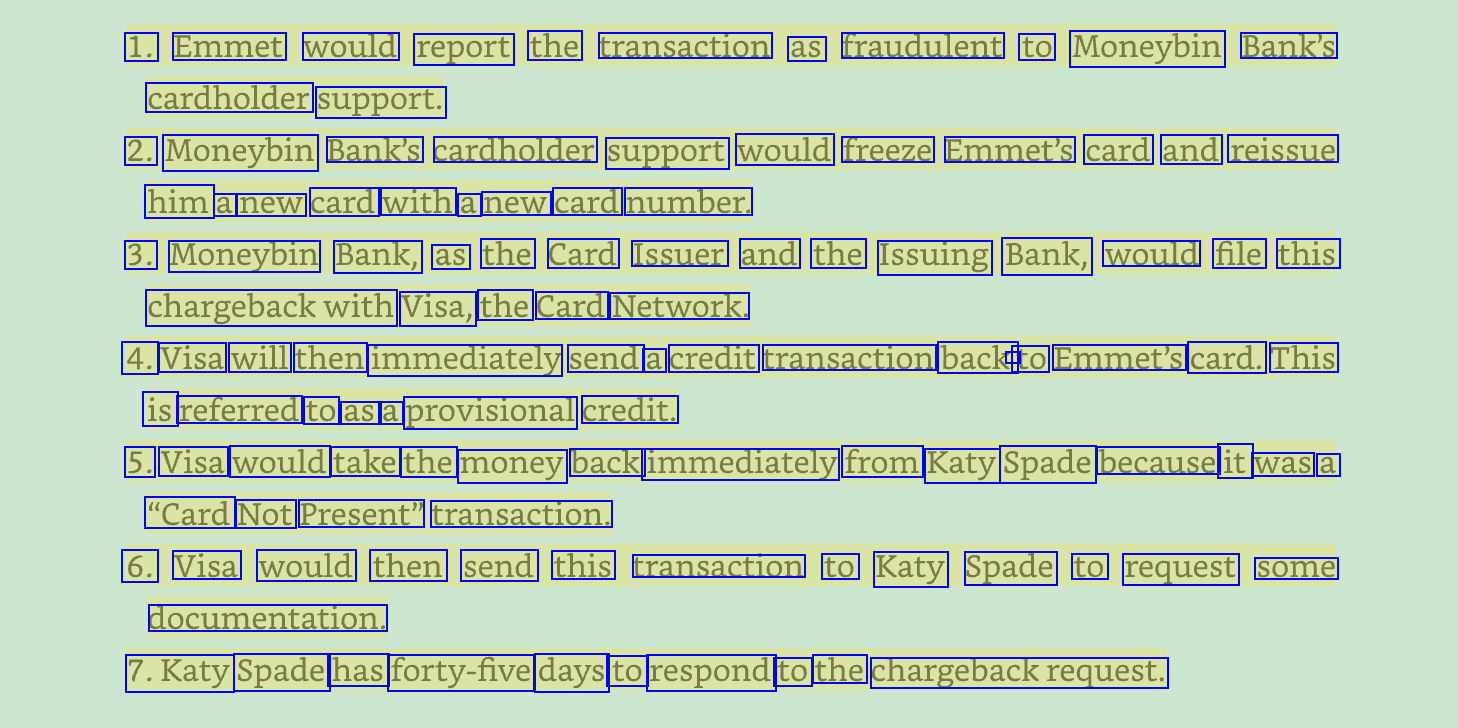

1. Emmet would report the transaction as fraudulent to Moneybin Bank's cardholder support. 2. Moneybin Bank's cardholder support would freeze Emmet's card and reissue him a new card with a new card number. 3. Moneybin Bank, as the Card Issuer and the Issuing Bank, would file this chargebackwith Visa, the Card Network. 4. Visa will then immediately send a credit transaction back - to Emmet's card. This is referred to as a provisional credit. 5. Visa would take the money back immediately from Katy Spade because it was a "Card Not Present" transaction. 6. Visa would then send this transaction to Katy Spade to request some documentation. 7.Katy Spade has forty-five days to respond to the chargebackrequest.

2023-07-02_14-04-37_screenshot.png #

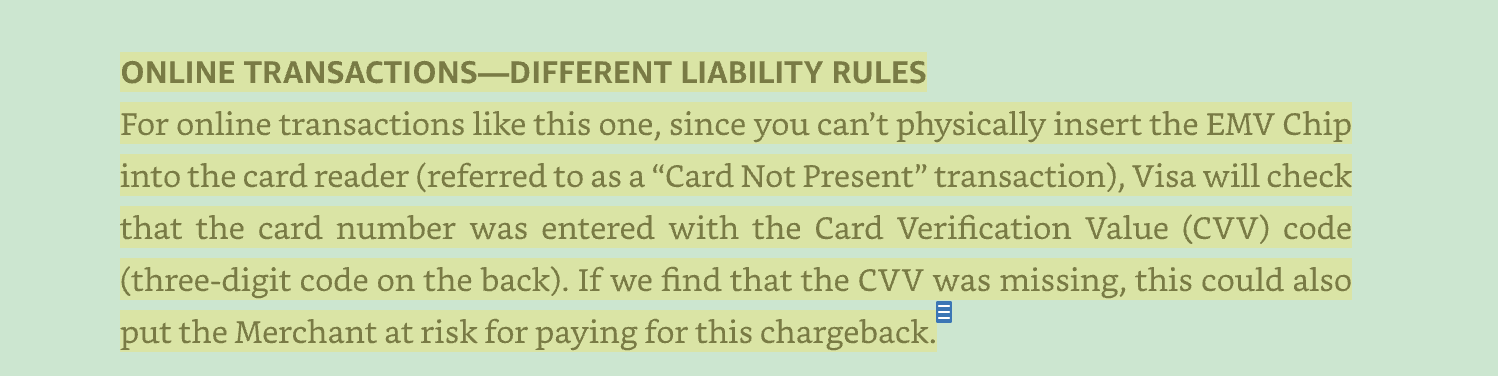

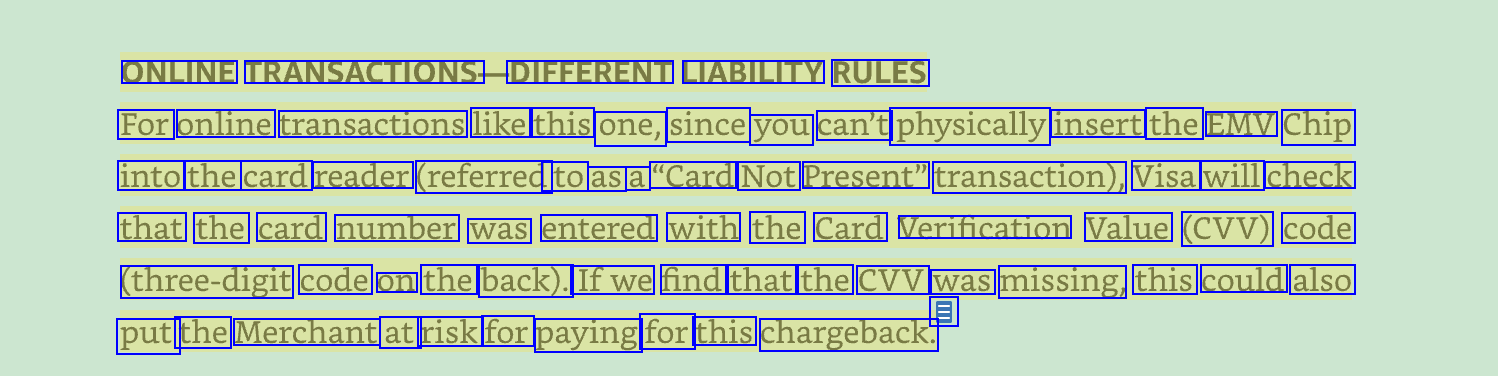

ONLINE TRANSACTIONS: DIFFERENT LIABILITY RULES For online transactions like this one, since you can't physically insert the EMV Chip into the card reader (referred to as a "Card Not Present" transaction), Visa will check that the card number was entered with the Card Verification Value (CVV) code (three-digit code on the back). Ifwe find that the CVV was missing, this could also E put the Merchant at risk for paying for this chargeback.

2023-07-02_14-04-57_screenshot.png #

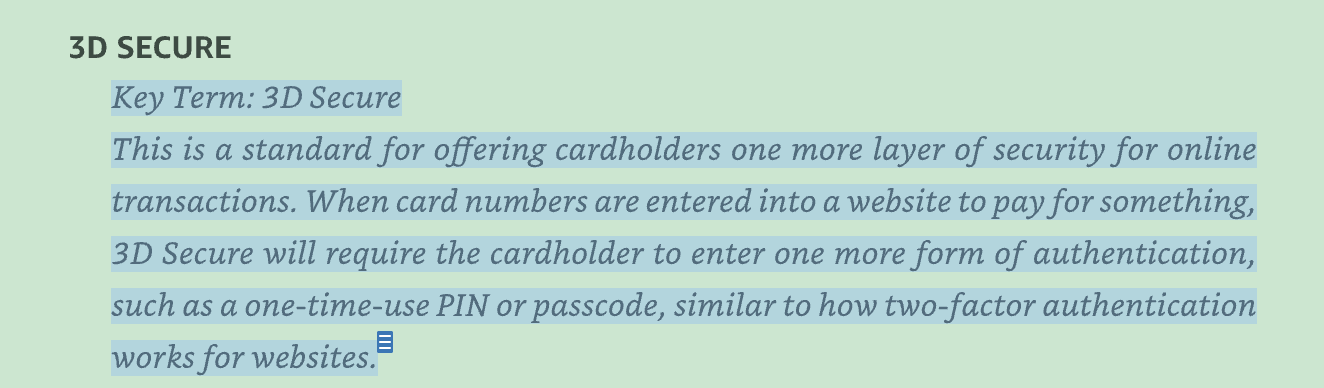

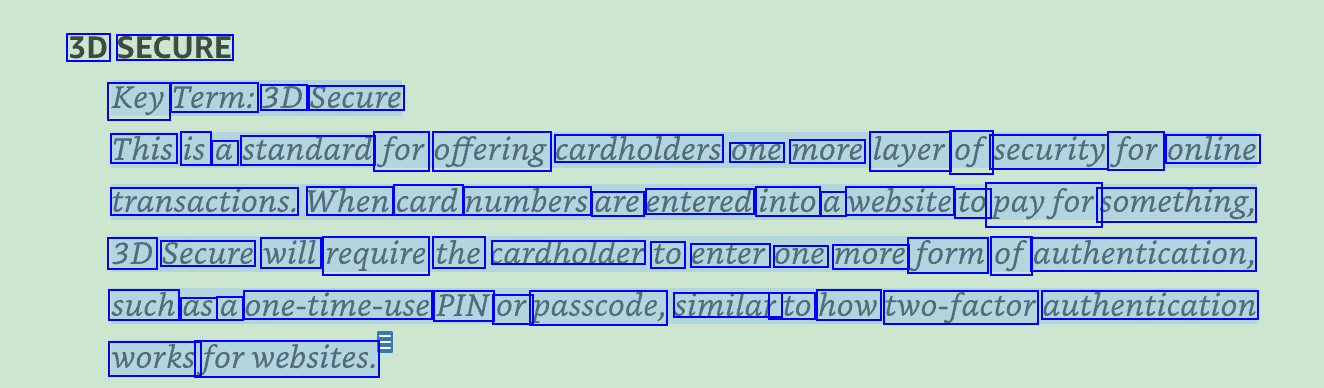

3D SECURE Key Term: 3D Secure This is a standard for offering cardholders one more layer of security for online transaction.s. When card numbers are entered into a website to payfor something, 3D Secure will require the cardholder to enter one more form of authentication, such as a one-time-use PIN Or passcode, similar to how two-factor authentication works forwebsites.

2023-07-02_14-05-36_screenshot.png #

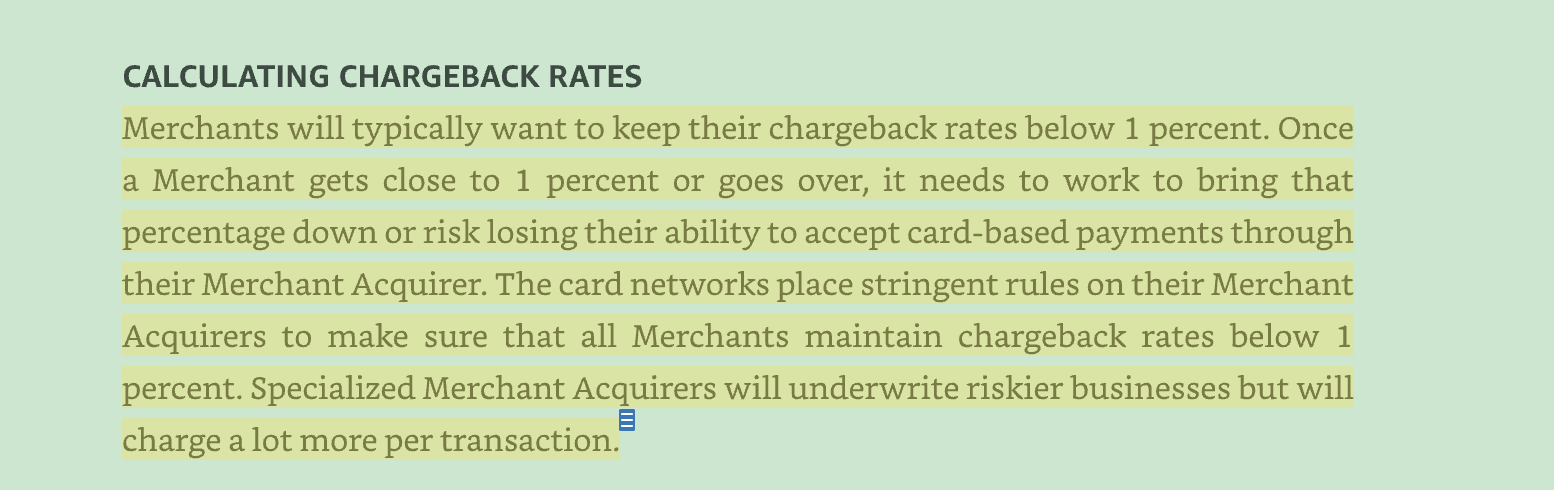

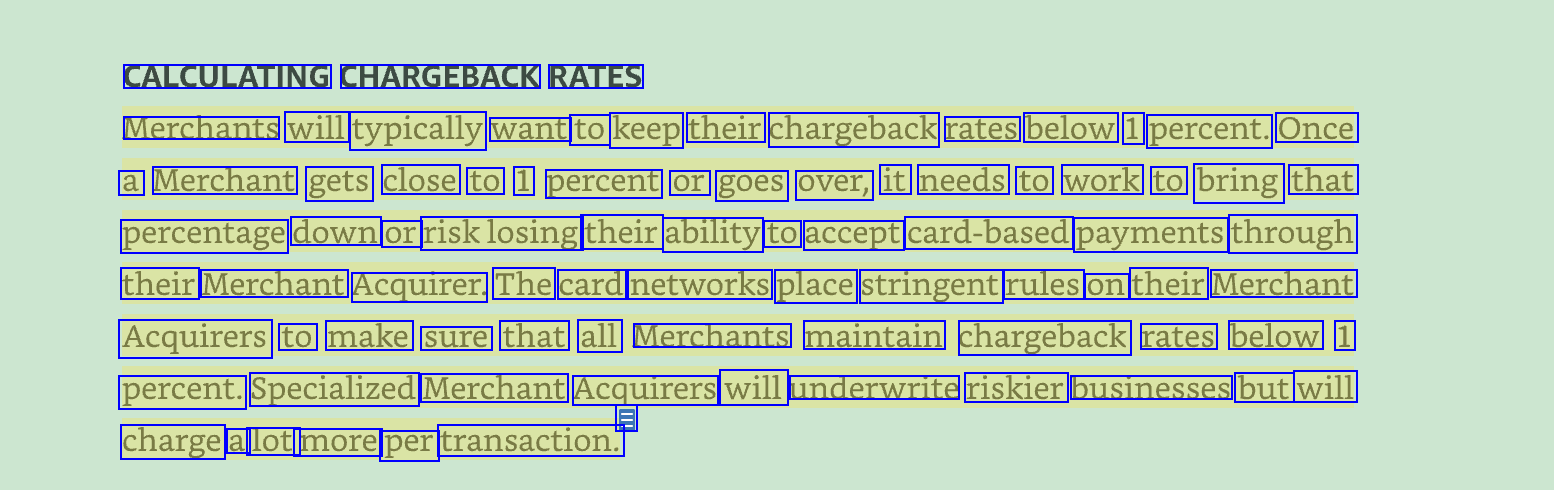

CALCULATING CHARGEBACK RATES Merchants will typically want to keep their chargeback rates below 1 percent. Once a Merchant gets close to 1 percent or goes over, it needs to work to bring that percentage down or risklosing their ability to accept card-based payments through their Merchant Acquirer. The card networks place stringent rules on their Merchant Acquirers to make sure that all Merchants maintain chargeback rates below 1 percent. Specialized Merchant Acquirers will underwrite riskier businesses but will E charge a lot more per transaction.

2023-07-02_14-05-58_screenshot.png #

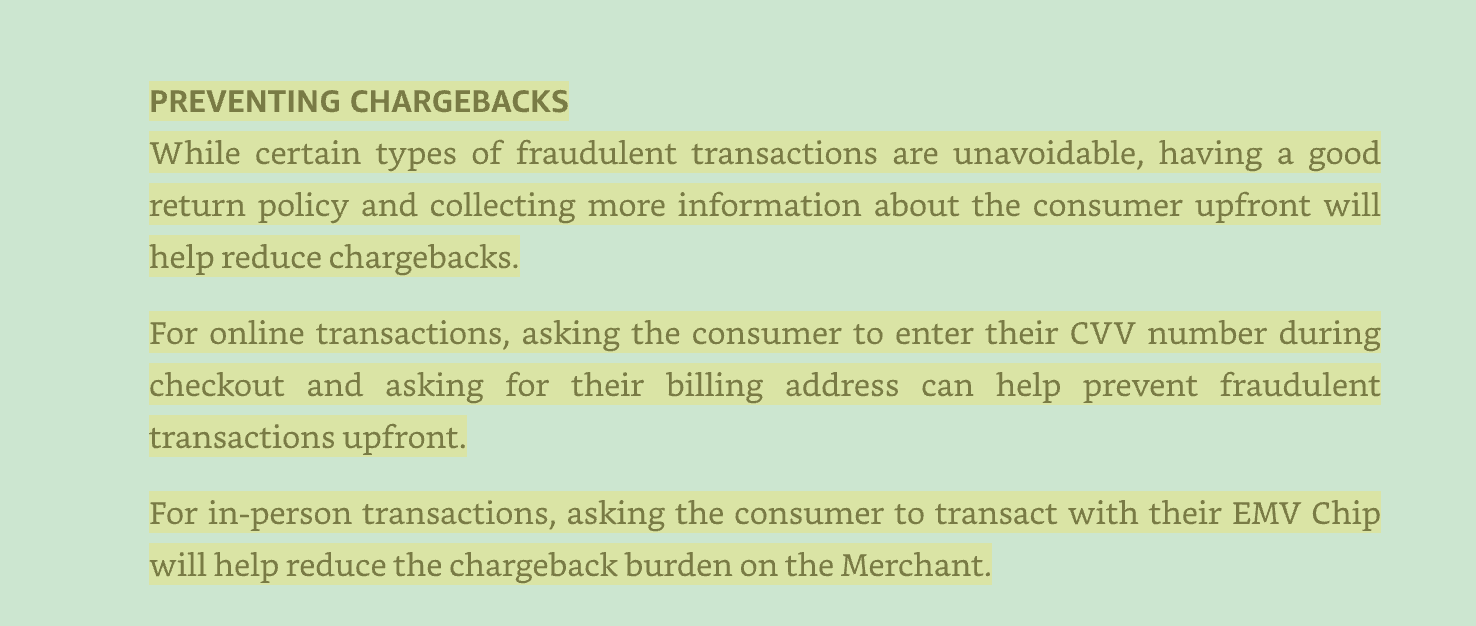

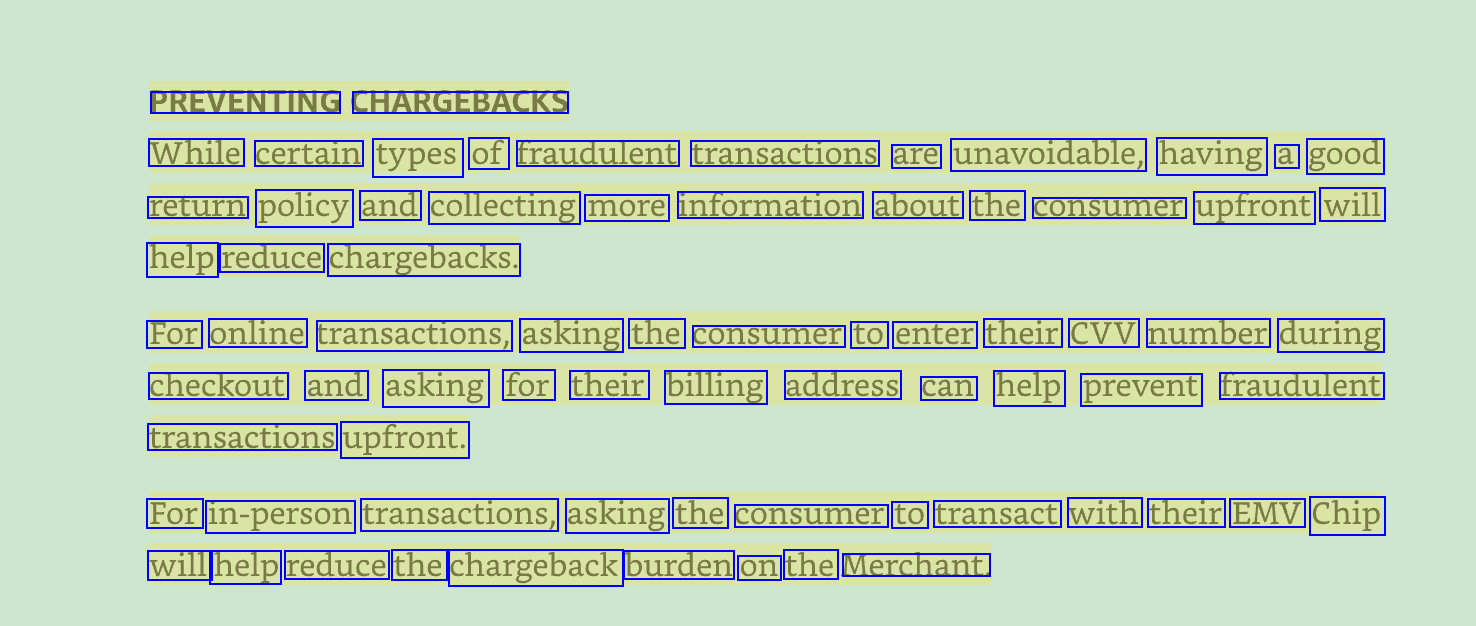

PREVENTING CHARGEBACKS While certain types of fraudulent transactions are unavoidable, having a good return policy and collecting more information about the consumer upfront will help reduce chargebacks. For online transactions, asking the consumer to enter their CVV number during checkout and asking for their billing address can help prevent fraudulent transactions upfront. For in-person transactions, asking the consumer to transact with their EMV Chip will help reduce the chargeback burden on the Merchant.